The Solar Bill Swap: Why Paying the Same Amount Is Still a Smart Move

Ready to find your true lowest rate?

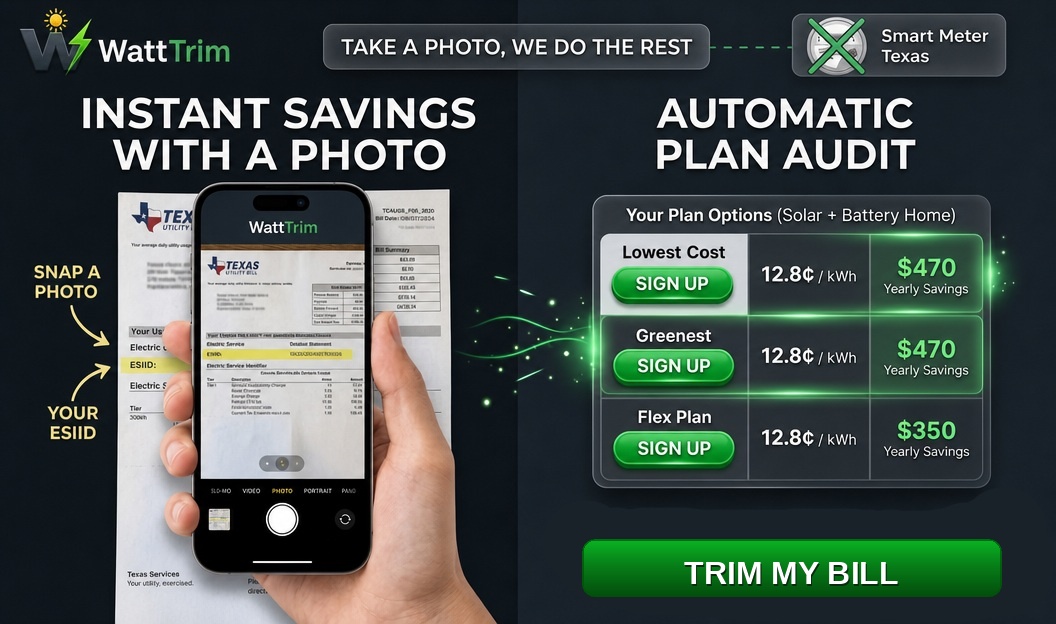

Snap a photo of your electricity bill and get a personalized analysis within minutes.

There's a moment in almost every solar consultation where the homeowner squints at the numbers and says, "So I'm paying roughly the same amount per month... why would I bother?"

It's a fair question. If your current electric bill is $180 and your solar loan payment would be $175, the monthly cash flow looks like a wash. Some people walk away at that point, thinking solar "doesn't make sense" for them.

But that thinking has a blind spot - and it's a big one.

Expense vs. Asset: The Core Distinction

Every month you pay your electric bill, that money is gone. You're renting electricity. You don't accumulate anything. Next month, you pay again. The year after that, you pay more - because rates go up.

A solar loan payment, even at the same dollar amount, is fundamentally different. You're purchasing an asset that sits on your roof, generates power for 25-30 years, and adds measurable value to your home.

Same monthly number. Completely different financial category.Think of it this way:

| Electric Bill | Solar Loan Payment | |

|---|---|---|

| What you're doing | Renting electricity | Buying equipment you own |

| Where the money goes | Utility company's revenue | Your home's equity |

| What you own afterward | Nothing | A power-generating asset |

| What happens when it's paid off | You keep paying forever | Your electricity is nearly free |

| Effect on home value | None | Increases resale value |

The Payoff Moment

A solar loan typically runs 15-25 years depending on the terms. The panels themselves last 25-30 years, sometimes longer. That gap is where the math gets exciting.

Let's say you finance a system with a 20-year loan at $175/month. For those 20 years, your cost is roughly the same as your old electric bill. But in year 21, your loan is paid off - and the panels keep producing.

Your electric bill drops to near zero. You're generating your own power from equipment you fully own.Meanwhile, your neighbor who stuck with the utility? They're still paying - except now their bill is higher because electricity rates have been climbing 2-4% per year for the past two decades.

Here's what that looks like over 30 years with a $180/month starting bill and 3% annual rate increases:

| Year | Utility Customer Pays (Cumulative) | Solar Owner Pays (Cumulative) |

|---|---|---|

| Year 10 | $24,800 | $21,000 |

| Year 20 | $58,100 | $42,000 |

| Year 25 | $80,600 | $43,200 |

| Year 30 | $108,400 | $44,400 |

Your Home Gets More Valuable

Multiple studies, including research from Zillow and the Lawrence Berkeley National Laboratory, have found that solar panels increase a home's resale value. The commonly cited figure is a 3-4% increase in home value, though it varies by market.

In Texas, where electricity costs are a visible monthly pain point, a home that generates its own power is a tangible selling point. Buyers see it as one less bill to worry about.

Even if you sell before the loan is paid off, the increased home value can offset or exceed the remaining loan balance - especially as the system ages and proves its output over time.

Rate Inflation Is the Silent Variable

Texas electricity rates aren't fixed across time. They fluctuate year to year, and the long-term trend is upward. The average residential rate in Texas has risen roughly 2-4% annually over the past decade, with sharper spikes during high-demand summers.

When you lock in a solar loan, your payment is fixed. Month 1 costs the same as month 180. Meanwhile, the electricity you would have been buying gets more expensive every year.

The "bill swap" that looks even today becomes a bargain five years from now - and a significant advantage ten years out.This is the part most quick comparisons miss. They compare today's electric bill to today's loan payment as if both numbers stay frozen. They don't. One is locked. The other drifts upward.

What About the Loan Interest?

Fair point. You're paying interest on a solar loan, which means the total cost over the life of the loan exceeds the panel price. But consider:

- You'd be paying the utility company anyway - and getting zero equity for it

- Solar loan interest rates are often competitive (5-7% for strong credit), and the interest may be tax-deductible depending on how the loan is structured

- The panels generate value every single day - unlike a car loan where the asset depreciates, solar panels produce a measurable financial return throughout their life

When the Bill Swap Doesn't Work

To be fair, this isn't a universal win. The bill swap makes less sense if:

- Your roof needs replacement soon - panels should go on a roof with 10+ years of life left

- You plan to move within 2-3 years - the equity benefit needs time to materialize

- Your electricity usage is very low - if your bill is already $60/month, the system size needed may not justify the installation cost

- Heavy tree shading - panels need consistent sun exposure to hit their production estimates

The Mindset Shift

The biggest barrier to solar adoption isn't the math - it's the framing. When someone hears "your payment will be about the same," they hear "no benefit." But that's like saying buying a house has no benefit over renting because the monthly payment is similar.

The benefit isn't in the monthly number. It's in what that number is doing for you.- Paying a utility bill: funding someone else's infrastructure

- Paying a solar loan: funding your own

How to Know If the Bill Swap Works for You

The key variables are your current electricity usage, your roof's solar potential, and the loan terms available to you. A few hundred dollars difference in system sizing or a half-point change in interest rate can shift the breakeven timeline significantly.

The best starting point is understanding your actual usage patterns - not just your average monthly bill, but how your consumption varies across seasons. That's where real projections come from, not estimates based on square footage or zip code averages.

Ready to Find Your Best Plan?

Browsing plans is a great start - but every home uses electricity differently. WattTrim analyzes your actual Smart Meter usage data to find the cheapest plan for how you use power, not just a generic benchmark.

Run Your Personalized Audit →Put This Knowledge to Work

WattTrim reads your actual Smart Meter data and finds the cheapest plan for how you use electricity. Just snap a photo of your electricity bill, and your personalized results are ready within minutes.

Trim My Bill