How Banking Lenders Made Solar More Expensive for Americans

Ready to find your true lowest rate?

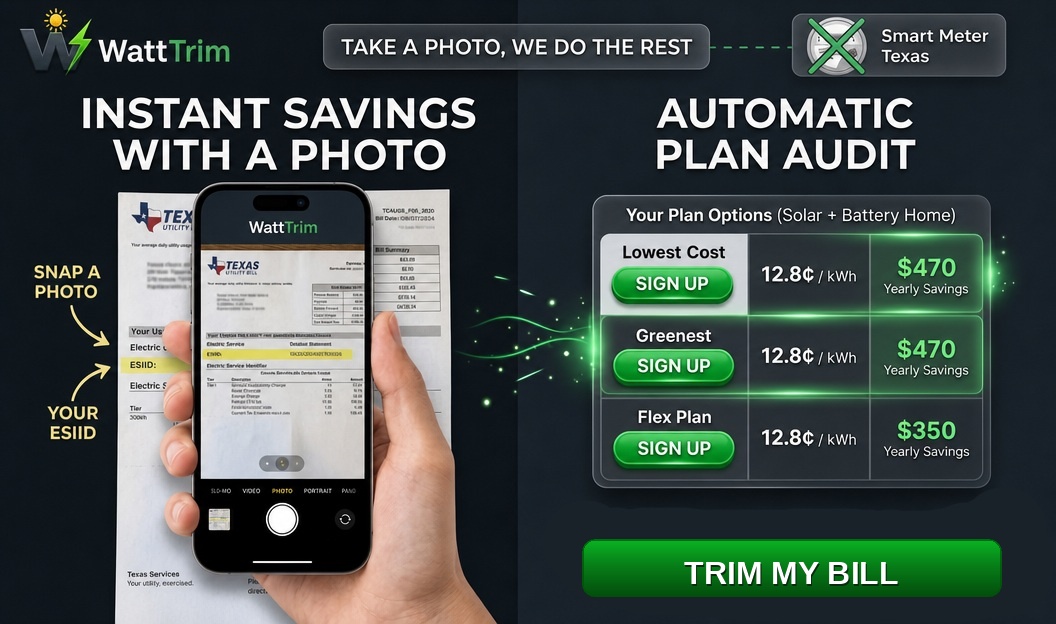

Snap a photo of your electricity bill and get a personalized analysis within minutes.

The $25,000 Question

The average residential solar installation in the United States costs about $25,000 before incentives. A comparable system in Australia costs around $6,000.

Same panels. Same inverters. Often the same manufacturers. Yet Americans routinely pay three times more for rooftop solar than Australians.

The difference is not sunshine. It is not labor costs. It is not the panels themselves.

The difference is what happens between the moment you say "yes" to solar and the moment you sign the loan.The Dealer Fee Machine

Here is how most residential solar sales work in America.

A salesperson knocks on your door or you respond to an ad. They quote you a system price -- say $30,000. They offer financing at an attractive rate, maybe 1.99% or even 0.99% APR over 25 years. That sounds reasonable. You sign.

What you probably do not know is that your $30,000 system just became a $39,000 loan.

The extra $9,000 is called a "dealer fee." The solar installer pays it to the lender in exchange for offering you that low interest rate. But the fee does not come out of the installer's pocket. It gets rolled into your loan principal. You finance it. You pay interest on it. And in most cases, nobody tells you it is there.

The Consumer Financial Protection Bureau (CFPB) investigated this practice and found that dealer fees routinely increase loan costs by 30% or more above the cash price. Some loans included markups exceeding 50% of the original system cost.

These are not edge cases. According to climate-focused lender Climate First Bank, dealer fees currently range from 20% to 40% across the industry. And most solar lenders contractually require installers to hide them from customers.

How a Low Interest Rate Costs You More Than a High One

The math behind dealer fees is deliberately confusing. Consider two options for a $30,000 solar system:

| Scenario | Loan Amount | Interest Rate | Total Paid Over 20 Years |

|---|---|---|---|

| Dealer fee loan | $39,000 (30% markup) | 1.99% | ~$47,200 |

| No-fee loan | $30,000 | 6.99% | ~$46,500 |

This is not an accident. The entire model is designed to make a bad deal look attractive by burying the real cost where you cannot see it.

Meanwhile, in Australia

Australia has the most successful rooftop solar market on earth. More than one in three homes has solar panels installed. In South Australia, that number is above 40%.

The national average installation cost is $0.89 per watt (AUD) -- about $5,300 for a typical 6 kW system. In the US, the median is $2.80 per watt, roughly $16,800 for the same size system before incentives.

Why such a dramatic gap?

No dealer fee financing model. Australian homeowners typically pay cash, use standard home loans, or take advantage of government interest-free loan programs. There is no parasitic lending layer extracting 30% of every project. Streamlined permitting. In many Australian states, a residential solar permit can be approved through an app within 24 hours. In the US, permitting alone can take weeks or months, require structural engineering reviews, and cost $1,000 or more in fees. Massive competition. With a third of households already on solar, Australia has a huge pool of experienced installers competing on price. Customer acquisition costs are a fraction of what US installers spend on door-to-door sales teams and digital marketing. Lower soft costs across the board. Inspection, interconnection, and regulatory compliance add thousands of dollars to US installations that simply do not exist at the same scale in Australia.The result: an Australian homeowner can install solar and pay it off in 3 to 4 years from energy savings alone. An American homeowner often faces a 10 to 15 year payback -- and that is if the dealer fees did not eat their savings entirely.

The Tax Credit Was Supposed to Help

For years, the US offered a 30% federal Investment Tax Credit (ITC) on residential solar installations. On a $30,000 system, that was a $9,000 credit.

Sound familiar?

The CFPB and multiple state attorneys general pointed out what many in the industry already knew: dealer fees were sized to capture the entire tax credit. The homeowner claimed 30% back from the IRS, and 30% had already been added to their loan principal. The credit effectively flowed straight to the lender.

It gets worse. The IRS explicitly states that financing fees are not eligible for the solar tax credit. But because dealer fees are rolled into the system price on paper, homeowners unknowingly claimed them as part of the installation cost. The lenders designed it that way.

The solar lender Mosaic, one of the largest in the country, filed for bankruptcy in 2025 after facing lawsuits over its lending practices. Minnesota Attorney General Keith Ellison sued four solar lending companies for deceptive practices, saying lenders "pocketed the fees, canceling out incentives for solar panel purchases."

And now the federal tax credit is gone.

What Happens Without the Safety Net

With the 30% ITC no longer available, the dealer fee model is under serious strain.

When the tax credit existed, homeowners could at least partially offset the inflated loan principal. Without it, a $30,000 system with a 30% dealer fee is simply a $39,000 debt -- with no $9,000 check from the IRS to soften the blow.

The industry now faces a choice: eliminate dealer fees and bring actual costs down, or watch adoption collapse as homeowners do the math and walk away.

Some lenders are already pivoting. LoanTERRA, a Seattle-based company, launched a platform to let credit unions originate solar loans directly -- no dealer fees, no middlemen. As their CEO Bill Paulen told ImpactAlpha: "The downside of the investment tax credit is there has been extra fat available, and that is how these dealer fees have been able to survive so long, in such magnitudes."

But the large fintech lenders -- the ones who built their business models on hidden fees -- are not going quietly.

What Texas Homeowners Should Know

Texas is one of the most active residential solar markets in the country. It is also ground zero for solar lending complaints. Thousands of Texans have filed complaints about misleading solar contracts, and regulators have taken notice.

If you already have solar in Texas, you may have a dealer fee buried in your loan. If you are considering solar, here is what to watch for:

Ask for the cash price. Then ask what the financed price would be. If there is a meaningful difference, the gap is almost certainly a dealer fee. Compare total cost, not monthly payments. A low monthly payment stretched over 25 years often costs far more than a higher payment over 10 years. Get multiple quotes. The variation in pricing between installers is enormous, partly because different companies absorb or pass through dealer fees differently. Read the loan documents carefully. Look for "origination fee," "program fee," "platform fee," or "original issue discount." These are all names for the same thing. Consider paying cash or using a home equity loan. A standard HELOC at 7% on $30,000 is almost always cheaper than a 1.99% solar loan on a $39,000 inflated principal.The Bigger Picture

Americans are not paying more for solar because the technology is expensive. Panels are a global commodity -- the same modules manufactured in China end up on rooftops in both Sydney and San Antonio.

Americans are paying more because a financing layer was designed to be invisible, and regulators were slow to catch up.

Australia did not build the cheapest rooftop solar market in the world by subsidizing panels. They did it by removing friction -- simple permits, transparent pricing, competitive installation markets, and straightforward financing. No hidden fees. No middlemen extracting a third of every project.

The technology is ready. The demand is there. What is missing in America is a financing model that works for homeowners instead of against them.

Where WattTrim Fits In

WattTrim was built on the belief that Texas homeowners deserve transparent, independent information about their electricity costs -- and that belief extends to solar.

If you already have solar panels and may be carrying a dealer-fee-inflated loan you did not know about, the best way to maximize your investment is to make sure you are on the right electricity plan. A solar buyback plan that actually pays you fairly for your exported energy can offset hundreds of dollars a year. WattTrim analyzes your actual Smart Meter data to find the best plan for your usage pattern.

If you are considering solar, our Solar Feasibility Study uses your real usage data to estimate what solar would actually save you -- without the inflated numbers and without the sales pitch.

No kickbacks. No provider deals. Just the math.

Ready to Find Your Best Plan?

Browsing plans is a great start - but every home uses electricity differently. WattTrim analyzes your actual Smart Meter usage data to find the cheapest plan for how you use power, not just a generic benchmark.

Run Your Personalized Audit →Put This Knowledge to Work

WattTrim reads your actual Smart Meter data and finds the cheapest plan for how you use electricity. Just snap a photo of your electricity bill, and your personalized results are ready within minutes.

Trim My Bill